By Marta Vilar – MADRID (Econostream) – The European Central Bank lagged markets in turning hawkish after the Middle East conflict began and is already retreating from that stance, even as investors continue to price in two rate hikes for 2026, having only recently dropped expectations of an April move. This shift is clearly reflected in Econostream’s ECB Tone Meter and we explain it in this piece.

As the Middle East conflict unfolded, markets were quick to price in rate hikes, but the ECB took its time, as we explained here. The shift toward a more hawkish tone only came after its first post-war meeting on March 19, by which point the conflict had already been underway for several weeks.

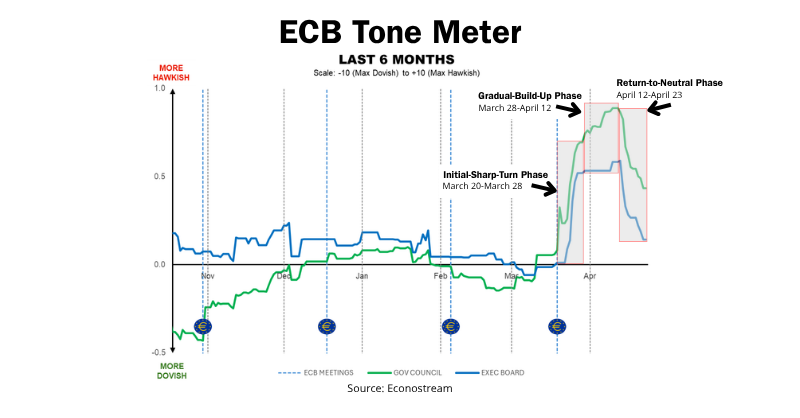

When it came, however, the shift was swift. The ECB Tone Meter rose from +0.08 (neutral) on March 19 to a peak of +0.89 by April 12 (still only slightly hawkish) in just over three weeks, before easing back to +0.44 by April 23—returning to neutral, just below the +0.5 threshold. In our framework (shown below), this reflects communication broadly consistent with unchanged rates in the near term, albeit with a slight tightening bias driven by the acknowledgement of upside inflation risks.

To explain what drove this shift, we break it down into three phases: an initial sharp turn (March 20–28), a gradual build-up (March 28–April 12), and a return to neutral (April 12–22).

Initial sharp turn (March 20–28)

The Governing Council index jumped from +0.08 to +0.69 in just eight days. Ahead of the March 19 meeting, policymakers had signaled only vague readiness to act. In its aftermath, they moved to explicitly acknowledge that hikes could become necessary if the outlook worsened, while also validating market expectations.

One of the most hawkish remarks since the ECB press conference came during this initial sharp-turn phase, when on March 20 Deutsche Bundesbank President Joachim Nagel said a rate hike would “probably be necessary” if inflation expectations rose—an outcome he described as “conceivable.”

At the same time, some policymakers began to openly validate market pricing. Central Bank of Ireland Governor Gabriel Makhlouf said on March 20 he could “well understand” why markets were anticipating two hikes, while Latvijas Banka Governor Mārtiņš Kazāks called such expectations “plausible.”

On March 24, incoming ECB Vice President Boris Vujčić pointed early to a shift toward more adverse scenarios. Meanwhile, ECB President Christine Lagarde moved beyond cautious signaling, warning on March 26 that a rapid return to normal was “overly optimistic” and that the shock could persist “for years,” implicitly pushing back against looking through it.

Still, rhetoric remained highly conditional. And while many policymakers had turned more hawkish, other voices continued to emphasize the possibility of looking through the shock, meaning no policy action. Banco de España Governor José Luis Escrivá was among the few making that case early on, on March 20.

More significant, however, were the remarks from Executive Board member Isabel Schnabel on March 27. Contrary to what her typically hawkish profile might have suggested, Schnabel said there was “no need to rush into action”, one of the earliest indications that an April rate hike was unlikely.

Gradual build-up (March 27-April 12)

The next phase was one of consolidation rather than escalation, with the Governing Council index rising more slowly from +0.69 to +0.89. By early April, most policymakers had already been scored as leaning hawkish. As a result, incoming remarks tended to reinforce—rather than intensify—that stance, which helps explain why the ECB Tone Meter rose more gradually.

Banque de France Governor François Villeroy de Galhau, who despite his dovish track record had consistently said the ECB would act if necessary, now struck a somewhat more hawkish tone on April 2 by acknowledging that “the next change in key interest rates is highly likely to be upwards,” reinforcing a tightening bias already signaled by others.

During this phase, the first signals emerged that April could be skipped in favor of June —an adjustment that, in our ECB Tone Meter, implies a less hawkish stance as tightening is pushed further out. Banka Slovenije Governor Primož Dolenc said that if there was not enough information by April 30, “probably it would be worthwhile to wait until June.” He was followed by National Bank of Belgium Governor Pierre Wunsch, who said that while an April hike was not excluded, a move would likely come in June if the conflict persisted.

At the same time, some remarks subtly tempered the narrative. ECB Vice President Luis de Guindos noted on April 10 that no inflationary spiral had emerged yet and expectations remained anchored, while acknowledging that the ECB was moving away from its baseline and closer to the adverse scenario. This served as a reminder that, although risks were tilted to the upside, they had not yet materialized.

Taken together, these comments kept the tone on a slightly hawkish footing—but crucially did not mark an escalation from earlier rhetoric.

Return to neutral (April 12-22)

The move back toward neutral was more decisive, with the Governing Council index falling from +0.89 to +0.44. Policymakers’ comments during this period were scored less hawkish as they continued to outline conditions for hikes, but increasingly paired them with explicit calls for patience, especially regarding April.

Schnabel set the tone on April 15, saying the ECB could “afford to take the time” to assess the shock, reinforcing the patient stance she had signaled on March 27. Also on April 15, Nagel pointed to well-anchored inflation expectations, weakening the immediate case for tightening he had opened the door to in late March.

By April 16, the message was clearer. Chief Economist Philip Lane said it was “too early to have anything too decisive,” while Villeroy called a focus on April “premature.” Policymakers were not dismissing hikes— but were increasingly emphasizing the need to wait for greater clarity—supporting less hawkish scores compared with the gradual build-up period.

That tone broadened further on April 17. Austrian National Bank Governor Martin Kocher said it “doesn’t make sense to pre-empt something that doesn’t happen later on,” while Nagel said in an interview with Econostream that the ECB did not “have to deliver on specific expectations,” pushing back against market pricing without closing the door to action.

By April 20, Lagarde anchored this shift at the top, saying that uncertainty about both the duration of the shock and its transmission “argues for gathering more information before drawing firm conclusions.” Two days later, the message became even clearer: Bank of Greece Governor Yannis Stournaras said “we should wait,” and Bank of Lithuania Governor Gediminas Šimkus reinforced that “we really shouldn’t” hike rates in April. Comments explicitly calling for a near-term hold are scored as neutral in our ECB Tone Meter.

What mattered for the ECB Tone Meter was this shift in balance. Conditional references to tightening remained, but they were no longer dominant, and hikes were no longer framed as a likely near-term outcome. As more policymakers emphasized waiting and uncertainty, the aggregate tone drifted back toward neutral—even as the option of future hikes stayed firmly on the table.

The Governing Council is now back in neutral territory, just shy of slightly hawkish. For the ECB Tone Meter to move higher again after the April 30 meeting, conditional support for a hike would need not only to re-emerge as the dominant signal, but also to be framed once again as a plausible near-term scenario, rather than being offset by calls for patience.