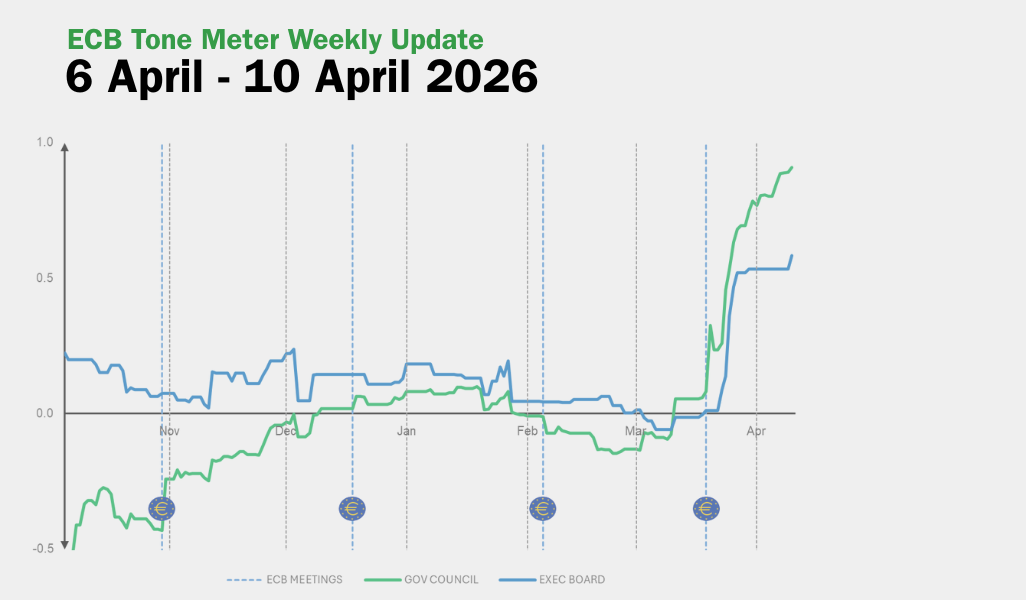

By David Barwick – FRANKFURT (Econostream) – European Central Bank Governing Council member François Villeroy de Galhau said on Thursday that it was too early to predict the timing of any ECB rate increase, but that the next move in rates was likely to be upward.

Villeroy, who heads the Banque de France, said in a speech at Sciences Po, “It is far too early to predict a timetable for ECB interest rate rises but it is clear that we have the capacity to act when and in whatever way necessary.” He added, “Obviously, the next change in key interest rates is highly likely to be upwards.”

The euro area was not facing a repeat of 2022, despite the new energy shock linked to the war in the Middle East, he said.

“Are we going through 2022 once again? The answer at this stage is no,” Villeroy said. He said the euro area was starting from a different macroeconomic position, with inflation at 1.9% in February 2026, versus 5.9% in February 2022.

At the same time, Villeroy said the conflict’s prolongation had moved the economy away from the central scenario of the ECB’s last projection exercise.

“As of today, 2 April, we are closer to the intermediate adverse scenario than to the baseline scenario adopted by the ECB on 19 March,” he said. He also said March inflation data showed “a strong first-round effect,” with higher energy prices lifting headline inflation while core inflation remained contained so far.

“Nevertheless, the utmost vigilance is required: market inflation expectations have risen sharply; we do not yet have those of businesses and households,” he said. “And our macroeconomic models may underestimate more negative microeconomic consequences: disruption to certain supply chains for plastics or other related products; and the temptation for companies – even in other sectors not directly affected by the initial shock – to ‘pre-empt’ price increases.”

According to Villeroy, the challenge is “to not let inflation get out of hand, whilst at the same time avoiding overreacting to a shock that is, in any case, already slowing down the economy.”

Rather than worrying about oil or gas prices per se, the ECB’s responsibility concerned “how this shock will – or will not – feed through to core inflation, expectations, financial conditions, and ultimately to price stability over the medium term,” he said.

The same three pillars as usual remained essential for the approach to monetary policy: the outlook for inflation including expectations; core inflation; and policy transmission, he said.

“In the face of the current supply shock, our focus is especially on the first two components,” he said. “Aside from the initial shock to energy prices, the key issue is the pass-through to the domestic components of inflation: wages, service prices, inflation excluding energy and food, and their future trajectory.”

He continued: “This is where persistence comes into play. We are therefore paying very close attention to firms’ price expectations, particularly through our Banque de France monthly business surveys, which are excellent indicators of the frequency and magnitude of price adjustments. We are also tracking the inflation expectations of households as well as wage indicators.”

Economic agents can however be confident, he said, noting the low sacrifice ratio of restoring euro area price stability between 2023 and 2025.

“And mark my words, this time even more so, we will act without haste but without any hesitation if this proves necessary,” he said.