By Marta Vilar – MADRID (Econostream) – Econostream’s ECB Tone Meter continued to move slightly higher this week for both the Governing Council and the Executive Board, even in the wake of the Middle East ceasefire.

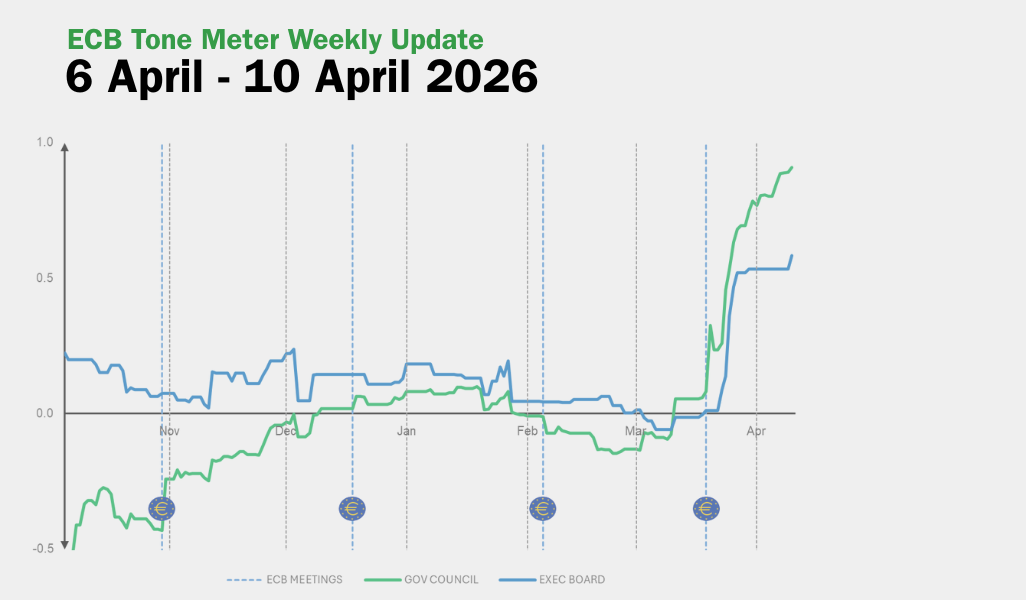

The Governing Council index climbed to +0.91 from +0.80, while the Executive Board index inched up to +0.58 from +0.54. Both gauges remain within the ECB Tone Meter’s “slightly hawkish” range, defined as between +0.5 and +2.5.

Policymakers this week appeared increasingly convinced that the outlook is shifting closer to the adverse scenario described in the ECB’s March projections. However, although they kept the option of an April rate hike on the table, they stopped short of actively signaling or stressing the possibility of such a move.

Regarding the ceasefire, only one policymaker discussed it in detail.

Biggest Movers of the Week: de Guindos, Wunsch and Sleijpen

ECB Vice President Luis de Guindos was the sole policymaker to provide detailed comments following the Middle East ceasefire. While he acknowledged that there may be doubts about the durability of the ceasefire, he balanced this by noting that it could open the door to dialogue between Iran and the US.

He also stressed that inflation expectations remain “relatively anchored” around the ECB’s 2% target. At the same time, he indicated that a peace agreement and the reopening of the Strait of Hormuz would bring the outlook closer to the ECB’s baseline scenario. This implies that, in the absence of such developments, the current situation is likely further from the baseline and potentially closer to a more adverse scenario.

National Bank of Belgium Governor Pierre Wunsch struck a relatively firm tone, indicating that a June rate hike would be necessary if the conflict were still ongoing. “If this is not done by June, I think we’re going to have to hike,” he said. Regarding April, he did not rule out a move but offered no further detail, suggesting he could accept holding steady then, but not delaying action beyond June if conditions remain unchanged.

De Nederlandsche Bank Governor Olaf Sleijpen also commented on the April meeting, noting that the available data would be “limited” by that point. Later in the week, he emphasized that the longer the conflict persists, the greater its impact on both inflation and growth. He added that the economy is already experiencing “significant hits” and warned that a prolonged period of elevated oil prices could lead to second-round inflationary effects.

Dominant Themes in This Week’s Communication: Growing Conviction Around a More Adverse Scenario

A key theme last week was the perception that the outlook was shifting away from the baseline toward more adverse scenarios, with Banca d’Italia Governor Fabio Panetta, Banka Slovenije Governor Primož Dolenc and Eesti Pank Governor Madis Müller all pointing in that direction.

This week, additional governors echoed that view. Bank of Lithuania Governor Gediminas Šimkus said the euro area is moving toward a less favorable scenario, while Bulgarian National Bank Governor Dimitar Radev noted a “higher likelihood” that a more adverse outcome could materialize.