Risk off mentality in the markets reached a recent peak on Friday with focus in particular on risks around the further spread of Coronavirus. At the close of Friday, OIS markets were predicting 2 full 25bp FOMC interest rate cuts over the next year (see below for a full explanation of what this means).

Markets have eased off these more extreme levels with two main events calming markets yesterday - reports of a research team at Zhejian University finding an effective drug to treat the Coronavirus and US ADP employment data printing at the highest since May 2015 at 291k.

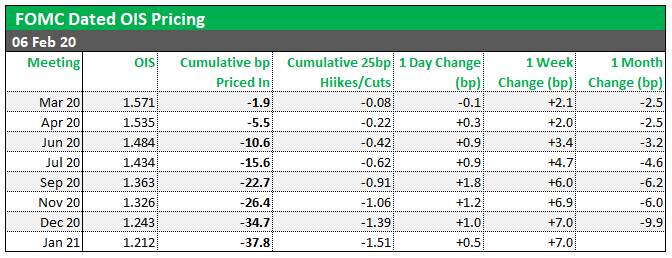

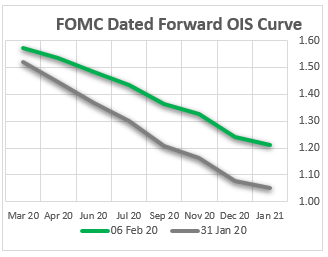

OIS markets are now only predicting a full FOMC 25bp cut by November, much later than the July prediction just late on Friday and now expect "just" 38bp of interest cuts over the next year (14bp less than late on Friday). ie markets still expect easing from the FOMC, but less and slower than just a few days ago.

The table and graphs show what the financial markets anticipate (or are “pricing in”) for future interest rate policy from the Federal Reserve’s FOMC – ie Fed Funds hikes and/or cuts - and how this has changed over recent days and weeks. This provides a great barometer of how the markets are interpreting the impact of recent news, speeches, data and events on the outlook for monetary policy.

To create the table we analyse the OIS markets (see details below). The table shows, for each future FOMC meeting: the level of the OIS market, how much that implies the FOMC rate will move up or down from current levels by the time of that meeting (in basis points) and how many hikes or cuts that is equivalent to. The table also details how much these expectations have changed over the last day, week and month.

If, for example, the table shows the FOMC will lower rates 12.5bp by the December meeting (ie half a 25bp cut), this implies the market thinks there is a 50% chance of an interest rate cut at, or before, the December meeting.

Interpreting the Data

There are a few different ways to determine what the market expects for future interest rates moves by central banks. All involve analysing short term interest rate markets and the options vary a little by country. We generally prefer using the OIS (overnight indexed swap) market - specifically the OIS swap dated to a specific central bank meeting. The dates on these swap contracts exactly match the central bank policy implementation dates allowing for an accurate reading. The difference between the interest rates implied by these OIS contracts and the actual current overnight interest rate can be interpreted as the expectations for the direction and magnitude for that central bank’s future interest rate policy change. For the FOMC we use FOMC Dated OIS contracts.