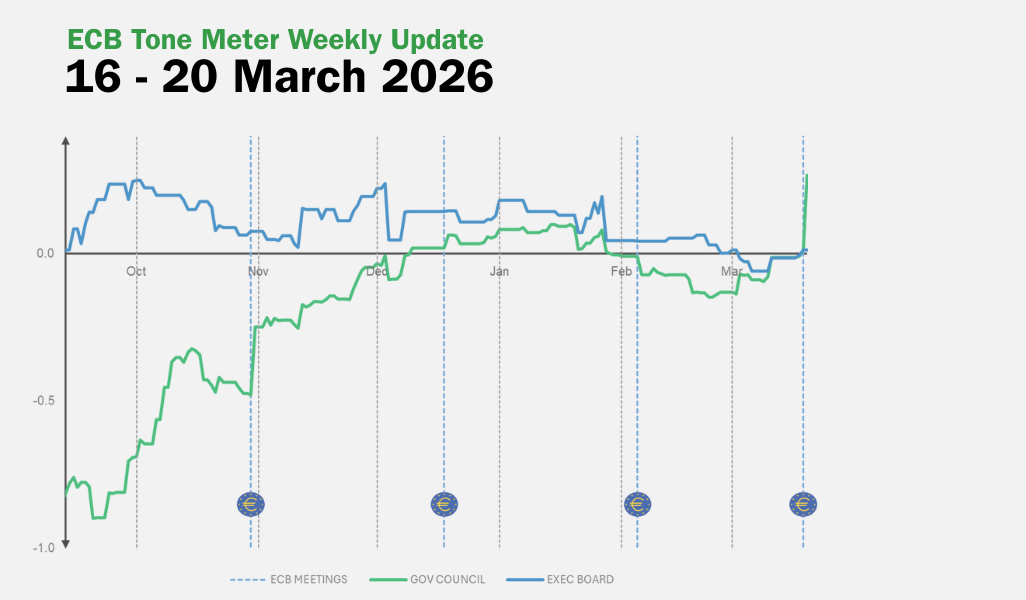

By David Barwick – FRANKFURT (Econostream) – After ascertaining on 01 August that the option of a pause at the 14 September meeting of the European Central Bank Governing Council had taken an early lead versus the lone alternative of yet another hike, we observe today that little has changed about this, which is not surprising, given that it also remains the case that monetary policy is still subject to the summer lull, leaving public pronouncements rare.

If we are not mistaken, only four Council members have spoken publicly since the beginning of the month. None of their comments call our previous analysis into question.

- ECB Chief Economist Philip Lane – new comments of his have been published three times in the form of podcasts that were actually recorded on 27 July. On balance, his remarks suggest that he would not be at the forefront of those wishing to hike again next month. ‘…one year into this hiking episode, it's clearly … starting to have a visible effect on the level of demand in the economy’, he said. ‘And this is really visible now, but I'm pretty sure it's going to deepen in the next number of months.’ Of course, we had already classified Lane as likely to be among those wishing to pause.

- Bundesbank President Joachim Nagel – in comments made today, Nagel was, if anything, just a touch more circumspect than he had been in his previous public statements a day after the 27 July Council meeting. Whilst reiterating some typical, rather hawkish messaging, he chiefly argued for awaiting incoming information before committing to any particular policy decision. We will naturally continue to consider him, as on 01 August, as more inclined to hike, but he left the door wider open than before to refraining from further tightening next month.

- Banco de Portugal Governor Mário Centeno – calling as he did yesterday for policymakers to be ‘cautious this time around because the downside risks that we identified in June in our forecast have materialised’ and describing it as ‘important to keep in mind that inflation has been falling faster than its way up’, we have no problem leaving him in the camp of those biased towards pausing, although like Nagel, he also made clear that the September decision would depend on all data available at the time.

- Croatian National Bank Governor Boris Vujčić – though generally hawkish, he was hardly chomping at the bit today to tighten official borrowing costs yet further. He seemed to be willing to leave things up to inflation readings yet to come before determining ‘whether we will really see a softening of the core inflation and inflation moving towards our target’, though at the same time, he suggested that a higher peak would allow earlier easing, and precisely in this context said, ‘the sooner we bring the inflation down, the better’. We leave him in the group of those whose bias is unclear.

We don’t necessarily expect ECB President Lagarde to fundamentally change prospects when she speaks late today by European time. It is simply the case that there are 20 days still to go until the Governing Council has to make a decision, with plenty of data yet to become available, including key spot inflation readings and the highly important updated staff macroeconomic forecasts. It would ill behoove her to be much less faithful to the data-dependent, meeting-by-meeting mode other Council members seem to be respecting.

In sum, we stick to the view expressed by us initially on 25 July that ‘we suspect it [the ECB] won’t’ hike in September. We can easily enough repeat now what we wrote two days later, namely that ‘there remains a non-negligible risk that the ECB will in fact hike. It is however also clear that the stage has been set for a pause, which for us at this point, as before today's press conference, is the likelier scenario.’

Of course, the final outcome will depend in part, as monetary authorities themselves underscore, on data not yet available. It is clear that an upside surprise in euro area HICP for August, for example, could harbour the potential by itself to sway the policy decision in another direction.

Here again are the details of how we think the individual members of the Governing Council are currently leaning with respect to the 14 September decision. As noted on 01 August, we took a prudent approach, leaving a plurality of Council members in the ‘unclear’ camp:

PAUSE (8 MEMBERS)

Ignazio Visco (Banca d’Italia)

Philip Lane (ECB)

Luis de Guindos (ECB)

Fabio Panetta (ECB)

François Villeroy de Galhau (Banque de France)

Yannis Stournaras (Bank of Greece)

Mário Centeno (Banco de Portugal)

Constantinos Herodotou (Central Bank of Cyprus)

HIKE (6 MEMBERS)

Isabel Schnabel (ECB)

Joachim Nagel (Bundesbank)

Pierre Wunsch (Belgian National Bank)

Mārtiņš Kazāks (Latvijas Banka)

Peter Kažimír (National Bank of Slovakia)

Robert Holzmann (Austrian National Bank)

UNCLEAR (12 MEMBERS)

Christine Lagarde (ECB)

Klaas Knot (De Nederlandsche Bank)

Tuomas Välimäki (Bank of Finland)

Madis Müller (Eesti Pank)

Boštjan Vasle (Banka Slovenije)

Gabriel Makhlouf (Central Bank of Ireland)

Gediminas Šimkus (Bank of Lithuania)

Boris Vujčić (Croatian National Bank)

Gaston Reinesch (Central Bank of Luxembourg)

Pablo Hernández de Cos (Banco de España)

Edward Scicluna (Central Bank of Malta)

Frank Elderson (ECB)