By David Barwick – FRANKFURT (EconoStream) – The European Central Bank’s monetary policy strategy review may turn contentious at times, given the range of Governing Council members’ perspectives, the review’s broad scope and the possibility its outcome will influence policy for decades. A heated debate about clarifying the symmetry of the ECB’s price stability definition may however be off the table following a single sentence uttered by ECB President Christine Lagarde on Wednesday.

Speaking at the ECB and its watchers conference about the review, she appeared to settle the issue by remarking that ‘to underpin inflation expectations, we need to ensure that our aim is perceived to be symmetric by the public.’

Such a denouement might seem inconsistent with other comments she has made since taking over the helm of the ECB last November. For example, a month after taking office, she told EU Parliament that symmetry was ‘clearly one of the items that will be debated as part of the strategic review’.

And only three weeks ago, following the September 10 monetary policy meeting, Lagarde declined to predict any outcome, saying, ‘I think it would be totally unwise and not loyal at all for me to already prejudge what the strategy review deliberations will be.’

But Lagarde is known to seek consensus, and if she chose to take the question of symmetry off the table at this early stage, it is less likely a contradiction of her own position in the form of an end run around potential opposition than it is an indication that she had already obtained the necessary backing – not simply to force symmetry through, but to be confident of not provoking an echo of discord.

To be sure, the opposition hasn’t been in the majority recently. A notable representative has nonetheless been Bundesbank President Jens Weidmann, who has highlighted the perception that the ECB’s inflation objective is worded inconsistently with a symmetrical definition.

‘Indeed, in conjunction with our definition of price stability, the formulation of the target to date is not symmetrical in my view’, he said in August of last year. ‘In principle, this can be discussed in a comprehensive strategy debate. In the current situation, this reinterpretation of the target would above all increase the pressure for monetary policy action.’

Weidmann last February expressed misgivings about the proposal ‘that emphasis be placed on symmetry’. This, he complained, ‘would increase pressure on monetary policymakers to take action.’

His opposition – let alone the reasons for it – doesn’t hold sway on the Governing Council, though it could suggest who may align how. A former Council member Econostream spoke to said that support for a clearly symmetrical definition of price stability ‘definitely’ mirrored hawk/dove fault lines. Yet, such a split may not really be a given; just last week, the Executive Board’s lone hawk, veteran Yves Mersch, said, ‘We always insist on symmetry.’

Mersch will retire at the end of this year, but among those to remain on the Board, no one appears to have recently voiced opposition to reinforcing symmetry, although Vice President Luis de Guindos said of the subject almost exactly a year ago that ‘while it’s not a minor question, it’s not the most important one either.’

Chief Economist Philip Lane, who could be expected to disproportionately affect the outcome of the review, has waxed markedly more enthusiastic about symmetry on repeated occasions. ‘Stating clearly our commitment to symmetry is important, since the formulation of our aim – “below but close to 2%” – risks being misunderstood, particularly in an environment of falling inflation expectations’, he said in September 2019. ‘[W]e care just as much about inflation too low as inflation too high’, he affirmed last November.

As for Weidmann’s colleagues on the broader Governing Council, Banque de France President François Villeroy de Galhau said on French television just four weeks ago that ‘you can be assured that a credible and symmetrical inflation objective will remain at the heart of our action.’

The fact that his countrywoman at the head of the ECB seems able to have fulfilled Villeroy’s promise without the distraction of a debate may be due in part to the current environment of low inflation – indeed, euro area HICP will likely be negative for a few months as of August.

The current inflationary circumstances are relevant because the way the price stability objective is now defined – ‘below but close to 2%’ – suggests, as the former Council member observed, that as a rule ‘they are worried more about higher inflation than lower’. But at present, deflation is a clearly larger threat than high inflation, potentially making symmetry easier to countenance for some.

Indeed, Weidmann’s opposition in February was partly predicated on the pre-pandemic assumption that things were going to get better, not worse. To embrace a clearly symmetrical definition of price stability was less appealing to him ‘at a time when the positive impacts of monetary policy actions on the real economy are potentially dwindling while risks and side effects are on the rise’, he explained at the time.

Another facet of the issue is the ECB’s communication on the matter; not long ago, the issue of symmetry flew largely under the radar. A casual observer might be excused for thinking it initially surfaced following the June 2019 monetary policy meeting of the Governing Council, when then-ECB President Mario Draghi somewhat tersely reported that ‘the conviction that we should pursue our objective in a symmetric fashion was also expressed’ during the gathering.

The subsequent publication of the meeting account showed that one or more members had argued that ‘the Governing Council’s communication should put more emphasis on the symmetry of its medium-term aim by clarifying that deviations of inflation … would be tolerated in a symmetrical fashion, in both directions’.

A few weeks after the June policy meeting, Draghi made use of the ECB’s annual conference at Sintra, Portugal to pave the way to such clarification. Curiously, he did so by essentially saying that such a shift to symmetry had already transpired five years earlier, evidently behind well-closed doors.

Speaking at Sintra on ‘Twenty years of the ECB’s monetary policy’, he recalled the steep decline in oil prices in mid-2014 and the subsequent weakening of inflation expectations, both of which occurred against a backdrop of already very low interest rates. The ECB’s reaction function had ‘needed to evolve to address these new challenges’, he explained.

Ensuring the ECB remained credible in the face of stubborn disinflationary pressures – a new situation for European monetary authorities – required first and foremost ‘clarifying the symmetry of our aim’, he told his listeners at Sintra, conceding that price stability’s ‘asymmetric formulation may have led to misperceptions in a low-inflation environment.’

The ECB in 2014 thus ‘made clear that our policy aim was fully symmetric, and it was symmetric around the level that we had established in 2003: below but close to 2%’, he recounted. ‘In addition’, he added, ‘we clarified that symmetry meant not only that we would not accept persistently low inflation, but also that there was no cap on inflation at 2%.’

Driving the point home, Draghi – still reminiscing at Sintra in June 2019 about what the ECB had done five years earlier - said symmetry ‘means that, if we are to deliver that value of inflation in the medium term, inflation has to be above that level at some time in the future.’

Soon after Sintra, in his introductory statement following the July 2019 monetary policy meeting, Draghi included for the first time the seven words that have since been part of every introductory statement and many speeches and interviews by Executive Board members: ‘in line with its commitment to symmetry’. In introducing the words, Draghi said he thought that he had ‘said this many times, but now it's in the introductory statement’.

As many or as few times as he had said it up to then, this commitment does not seem to have garnered much attention when supposedly made in 2014, at least not outside the Eurotower. To be sure, in February 2014 Draghi let drop somewhat en passant the comment that he ‘would still claim that we have a symmetric attitude’, which the ECB points to as evidence of an early commitment to symmetry.

In April 2014 he grew more direct. Speaking about ‘Monetary policy communication in turbulent times’ at the Dutch central bank, Draghi said: ‘… emphasis on the symmetry of our objective helps contain both inflationary and deflationary expectations.’ And during the Q&A after the March 2016 monetary policy meeting, he remarked that ‘[t]he key point is that the Governing Council is symmetric in the definition of the objective of price stability over the medium term.’

But the topic was doubtless overshadowed by the negative interest rate policy introduced in mid-2014 and quantitative easing starting in spring 2015. QE led to friction with the government of the ECB’s home country and biggest capital contributor, as well as with Weidmann. Why introduce another point of possible contention? The former Council member who spoke to Econostream said the subject of symmetry was ‘not that uncontroversial’.

It is thus hard to escape the conclusion, and easier to understand it, that the ECB had at least outwardly been oddly reticent until 2019 about symmetry. Perhaps for similar reasons, the subject may have had a hard time gaining traction within the Bank as well. The former central banker said that he recalled his Italian and Portuguese colleagues taking an interest in it, but not Draghi, who was disinclined to support a ‘proper, thorough discussion’ – even if he ultimately pushed the issue.

And after all, the architects of the ECB’s current monetary policy strategy had also not seen fit to dwell on the topic. Neither the slides nor the transcript of the press seminar on the evaluation of the ECB's monetary policy strategy on May 8, 2003 include a single mention of ‘symmetry’. Then-Chief Economist Otmar Issing came closest when he said, ‘We have both eyes – as Paul Samuelson said in a slightly different context – watching deflationary as well as inflationary developments.’

Still, since at least the July 2019 monetary policy meeting if not well before, symmetry seems to be a de facto if not a de jure element of the ECB’s view of price stability. Lagarde’s comment on Wednesday implies that the outcome of the strategy review will redress this imbalance. At a minimum, that should give the ECB more time to crack potentially harder nuts during the review process.

Latest News

Central Bank News

ECB Insight: Schnabel Gives the ECB Room to Wait

By David Barwick – FRANKFURT (Econostream) – European Central Bank Executive Board member Isabel Schnabel on Friday evening made a clear case for patience without remotely taking tightening off the table. Her core message was that the ECB should not let the memory of 2022 stampede it into treating every supply-side shock as the inevitable start of another inflation spiral, especially when the starting conditions—think today—are materially different.

27 March 2026

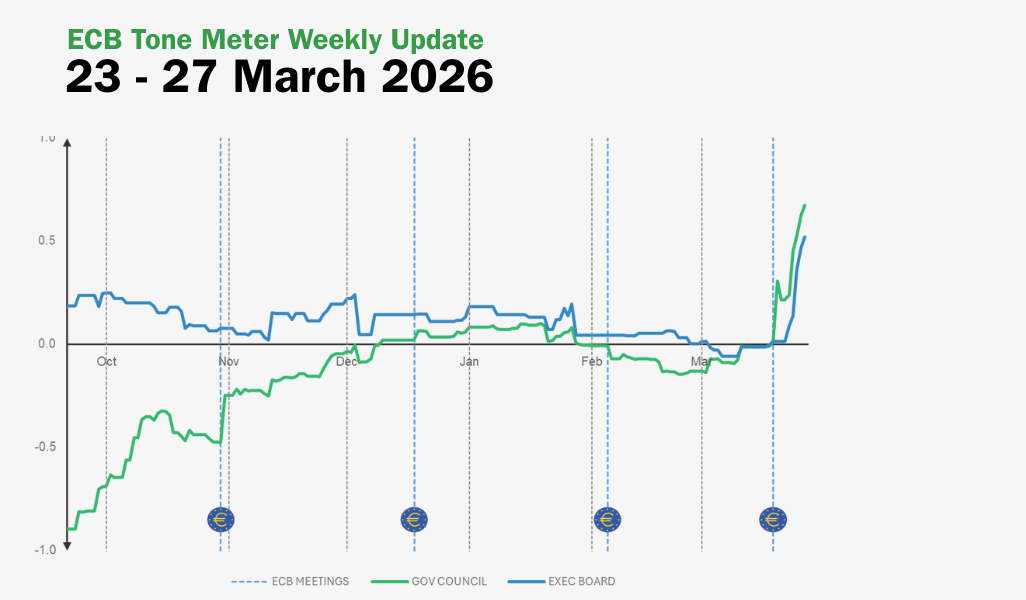

ECB Tone Meter Weekly Update: Governing Council and Executive Board Now "Slightly Hawkish"

By Marta Vilar – MADRID (Econostream) – Econostream’s ECB Tone Meter showed a notable shift in tone this week, with both the Governing Council and the Executive Board moving into what we classify as ‘slightly hawkish’ territory.

27 March 2026

ECB’s Schnabel: “There’s No Need to Rush into Action”

By Marta Vilar – MADRID (Econostream) – European Central Bank Executive Board member Isabel Schnabel said on Friday that policymakers should remain cautious in responding to the latest energy-driven inflation shock, adding that there was “no need to rush into action.”

27 March 2026Debt Issuance News

Transcript: Interview with KfW Head of Capital Markets Petra Wehlert on 20 March 2026

By Marta Vilar – MADRID (Econostream) – Following is the full transcript of the interview conducted by Econostream on 20 March 2026 with Petra Wehlert, Head of Capital Markets of KfW.

25 March 2026

Exclusive: KfW Head of Capital Markets: Euro Green Bond Issuance “Likely to Come Early” in Q2

By Marta Vilar – MADRID (Econostream) – German investment and development bank KfW is likely to issue another euro green bond in Q2 2026, according to KfW’s Head of Capital Markets, Petra Wehlert.

25 March 2026

Transcript: Interview with Swiss Federal Finance Administration’s Adrián Martínez on 13 March 2026

By Marta Vilar – MADRID (Econostream) – Following is the full transcript of the interview conducted by Econostream on 13 March 2026 with Adrián Martínez, Vice Director of the Swiss Federal Finance Administration.

18 March 2026